IRS - photo courtesy of alykat on Flickr.This is the team on the hot-seat-of-the-week. They’re the ones praying for a devastating tornado, locust outbreak, politician meltdown or the return of Jesus. Anything to get them off the front page and out of the crawl.

It’s the IRS office accused of unfairly scrutinizing and delaying applications for tax-exempt status from conservative political organizations like the Tea Party.

I don’t think the low-level staffers in the Determinations Unit were politically motivated. I think they were trying to deal with a mountain of work while understaffed, so they searched for keywords to aggregate applications and handle similar groups with a degree of regularity.

We’ve seen for years the unit is understaffed and struggles to keep up:

— application responses routinely take close to a year and I’ve known groups that waited months longer than that

— an online application project was delayed, and I haven’t heard about it since

— the 2011 loss of tax exempt status for 275,000 charities meant many thousands would reapply, adding monumental burden

Much is being made of the unit’s requests for donor lists, but how a group is funded has long been part of the criteria for determining whether an organization qualifies for tax-exempt status.

I’m looking at an IRS letter from 2001 confirming a client’s exempt status. The agency informs the organization that if its “sources of support, or its character, method of operations, or purposes have changed” there may be a change in the exempt status.

I predict this scandal will lead from IRS Code section 501(c)(4) to 501(c)(13): Cemetery companies owned and operated exclusively for the benefit of their members . . .

Then we’ll learn where the bodies are buried.

Updated June 6, 2013:

IRS released these FAQs on what the Determinations Unit did and why.

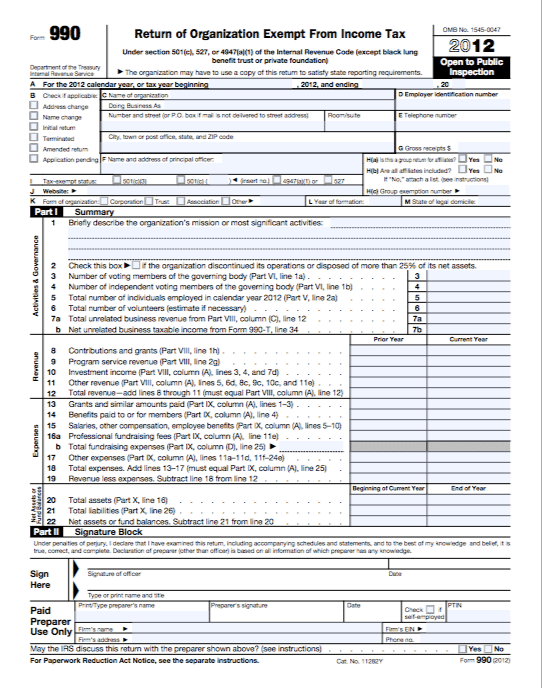

The form 990 filing deadline is four-and-a-half months after the close of your fiscal year. If your fiscal year ended on December 31, 2012, then your 990 is due by May 15th. The IRS expresses the deadline as “the 15th day of the fifth month” after close of your fiscal year.

Years ago, someone in a seminar was quite vociferous about how I was wrong to say four-and-a-half months. I couldn’t dissuade him. He wasn’t quibbling over “half a month” leading to the 14th of May.

He didn’t see the equivalence. I was polite.

Ninety-day extensions are granted automatically using form 8868. Typically charities need the extension because their previous year’s audit isn’t finished. Additional 90-day stretches aren’t hard to come by, but are not automatic. Use the same form, part II.

I’ve seen plenty of 990’s delayed for more than a year. That plays havoc, by the way, with charity registration deadlines in the states where you solicit donations. I know that work intimately. I wrote a book about it. I also published a paper.

Not sure which form to file (990, 990-EZ, 990-N postcard)? Here’s help.

Important fine print: I am not your attorney or your accountant. Seek the advice of your professional advisors in all matters of IRS compliance.

IRS building courtesy of Foist on FlickrThe IRS form 990 for 2012 has been released, and it continues to inquire about your office’s compliance with Charity Registration laws in the states where you solicit donations.

There have been significant changes to the form and its shorter sibling the 990-EZ.

But the Charity Registration inquiries remain.

Part VI, question 17 asks you to list the states in which you are required to file form 990. That is a basic part of registration in nearly every state. If you’re required to register before you solicit in a state, odds are you’ll be required to include the 990 with your application.

This is the federal agency’s oblique way of gaining jurisdiction–or legitimacy–to inquire about your compliance with state laws. It’s interesting.

Schedule G, part I, question 3 has you explicitly list the states in which you’re registered to solicit, or have been notified you’re exempt.

I hate to nitpick, but you won’t necessarily be notified by a state if you’re exempt there. In a good number of states, you determine exemption on your own and make no filing. In others you must file for exemption and be approved.

Every charity doesn’t submit this schedule with its 990. You file schedule G if, among other things, you spent more than $15,000 for professional fundraising services or reported more than that in fundraising event gross income. (See form 990, part IV, questions 17-19.)

Form 990 is signed by an officer under penalty of perjury. (See part II.)

There are precious few places where our IRS inquires about your compliance with state laws where you solicit donations.

But they’re alive and thriving.

If you want a fuller explanation of Charity Registration, take a look at the article I published in the journal “Taxation of Exempts.”

CMA Section: I am not your attorney or your accountant. Seek the advice of your professional advisors in all matters of IRS compliance.

Since June 2011 IRS has released a monthly list of charities whose tax-exempt status has been revoked for failure to file the annual form 990 or one of its smaller siblings, the 990-EZ and 990-N postcard, for three consecutive years.

This was big news when the automatic revocation list was inaugurated and close to 300,000 charities were revealed.

Next month’s list will be larger than usual because IRS is changing the admission standard. It’s easier to get on.

Starting in March, charities will get one month notice that they’re facing revocation. Until now, you didn’t make the list until tax-exempt status had been revoked for six months.

March’s list will have a seven month catch up–all those revoked but not yet revealed, plus those soon to be revoked–so it will be much longer.

I don’t understand why only one month of advance notice. Why not three or four months? That would presumably be enough time to make a 990 filing and avoid the revocation. One month isn’t enough time to pull it together.

In any case, expect a longer revocation list in March from IRS. There’s something to live for.

Courtesy of Philanthropy.comPassed on January 1, 2013, the American Taxpayer Relief Act of 2012 renewed charitable giving from individual retirement accounts (IRAs) for those 70-and-a-half or older.

If you were practicing Planned Giving a few years ago, this is deja vu. All the requirements are the same as in 2010, and there are two add-ons.

This is an IRA distribution, not a rollover. A rollover is a transfer from one retirement account to another retirement account.

What we have here is a distribution to charity. I use the vernacular in my title because that’s what people search for.

From here on I’m calling this a qualified charitable distribution, the exact designation in the Act.

Please recognize that my analysis is based on my reading of the American Taxpayer Relief Act of 2012, without the benefit of IRS rulings, tax court decisions or other official guidance that has yet to come. I am not providing tax, accounting or legal advice. Donors must consult their own advisors to determine whether, and how, to make a charitable gift.

Here are the requirements for a qualified charitable distribution:

Your donor is at least 70 1/2 years old on the date of gift and yours is a 501(c)(3) charity (supporting organizations are not included; nor are donor advised funds)

The IRA is a traditional or Roth

Maximum $100,000 per donor per year in qualified charitable distributions

The distribution is direct from IRA to charity

The full value of the gift would be eligible for an income tax charitable deduction if it were not a qualified charitable distribution

The amount distributed would be included in gross income if it were not a qualified charitable distribution

Promotion

Numbers 1-4 are straightforward and what I recommend using in promotional materials. Also drop in these two points if you have space:

First, the amount of the gift counts toward an IRA required minimum distribution, or RMD. Lots of people (though not as many as in 2007 and years before) are required to take more from IRAs than they need. This provision helps them reduce that dilemma.

Second, the amount of the distribution to charity is not included in federal gross income, so it’s exempt from federal income tax.

Important Fine Print

Numbers 5 and 6 have nuances that are more appropriate to an article than a blog. They are the primary reasons your materials include a disclaimer that you’re not providing tax or legal advice and donors must consult their own advisors. The first four are secondary reasons for your disclaimer, because there are ins-and-outs in those, too.

I will make an important point on #5. It precludes using this to buy a ticket to your dinner or an auction item; buy anything from your charity; or fund a charitable gift annuity or charitable trust. None of these are 100% deductible for federal income tax purposes. Raffle tickets are precluded because no part of the amount paid is a charitable contribution for federal income tax purposes. (They may be deductible losses if the person has gambling winnings, but we’re not going there.)

New From 2010

The two additions from the 2010 version are (subject to 1-6 above):

— Your donors can can make qualified charitable distributions before February 1 and count them toward 2012

— If donors took IRA distributions in December, they can count any portion of them as 2012 qualified charitable distributions. Their gifts need to get to you before February 1 to grab this opportunity. (You may disregard #4 for this.)

A Download For You

Here’s an easy one-pager I put together for you to share with your board; use in promo materials; excerpt for an email blast; carve up for a newsletter sidebar; and generally use for your charity as you like.

Getting Donors Started

It’s easy. They tell their IRA custodian they want to make a qualified charitable distribution to your charity. Share your tax ID number. Donors will need it to fill out a form.

Take advantage of this immediate-cash planned gift. It’s a valuable way to start the year and gives you a timely, newsy reason to talk to prospects.